The Great 2026 Inventory Pile-Up: What the Data Reveals About the Multi-Family Market

The first five months of 2026 have presented a puzzling paradox for the regional multi-family market. In a standard economic cycle, a surge in new listings is hailed as a sign of a healthy, liquid market. However, the data emerging from the first half of the year exposes a widening rift between seller optimism and buyer reality. While the volume of properties hitting the market has climbed aggressively, closed transactions have remained stubbornly stagnant. This is no longer a story of seasonal growth; it is a data-driven narrative of a market struggling to digest a sudden surfeit of supply.

The Widening Inventory Pile-Up

The defining characteristic of the 2026 market is the expanding chasm between inventory flow and buyer absorption. Known as Inventory Accumulation, occurs when the rate of new properties entering the market consistently outstrips the pace of sales, leading to a mounting backlog of unsold units.

YTD Inventory Pile-up: The expanding gap between new listings and stagnant sales volume demonstrates a clear trend of inventory accumulation throughout the year.

For investors, this gap serves as a vital warning light. When sales volume fails to track with listing growth, it typically signals a disconnect in valuation. The sheer weight of this accumulating inventory is beginning to shift the market’s center of gravity.

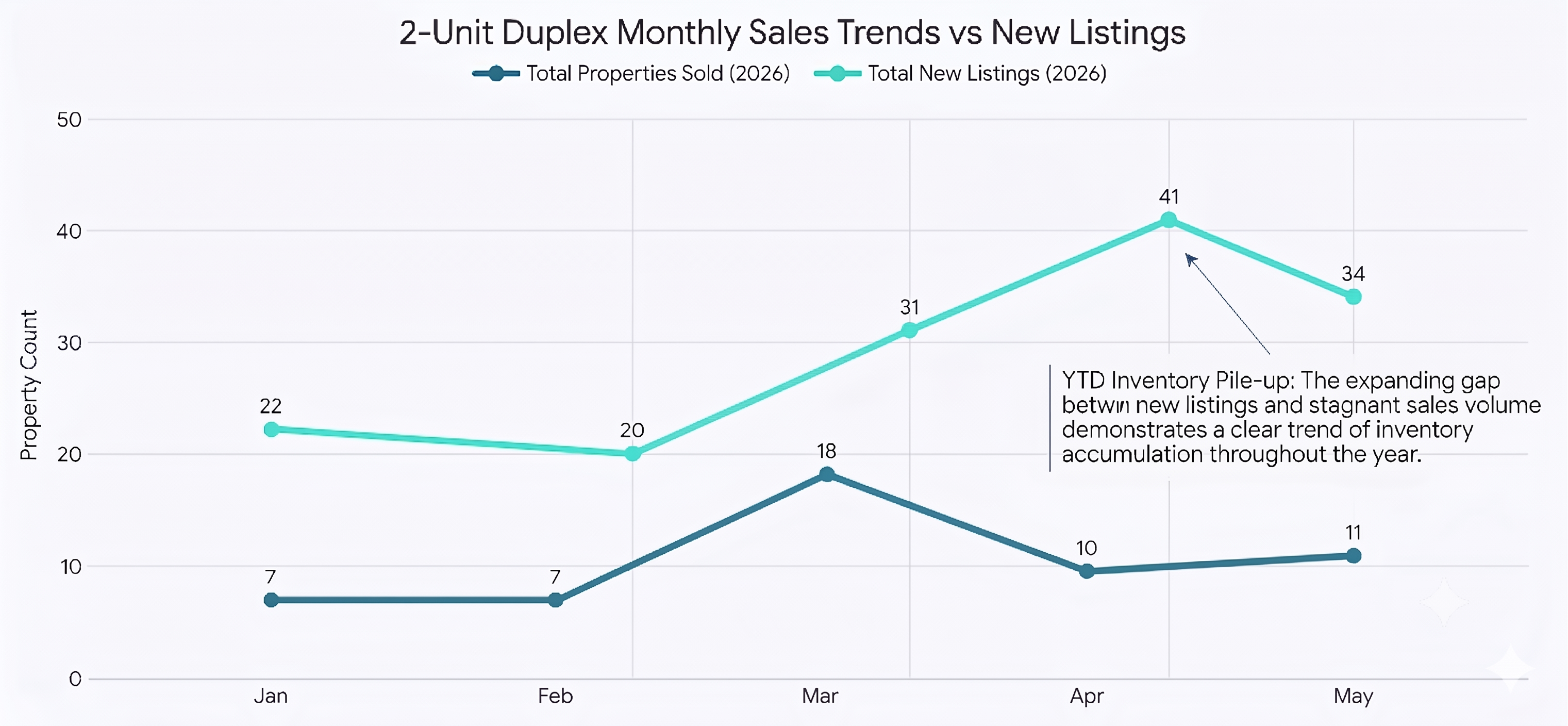

The Duplex Divergence: April’s High-Water Mark and the May Cooling

A MoM look at the 2-unit duplex segment reveals an increasing disparity in mid-spring. In April 2026, the market saw a high-water mark of 41 new listings, yet only 10 sales were finalized that month. That's a 4x1 ratio of listings coming into the market vs. sales.

While January began with a modest 7 sales, that figure only inched to 11 by May, trajectory that failed to mirror the supply side. Interestingly, new listings for duplexes saw a slight cooling in May, dropping from the April peak of 41 down to 34. However, because sales remained stuck at 11 units, the available inventory continues to grow; the backlog is not clearing, even as the pace of new entries slows.

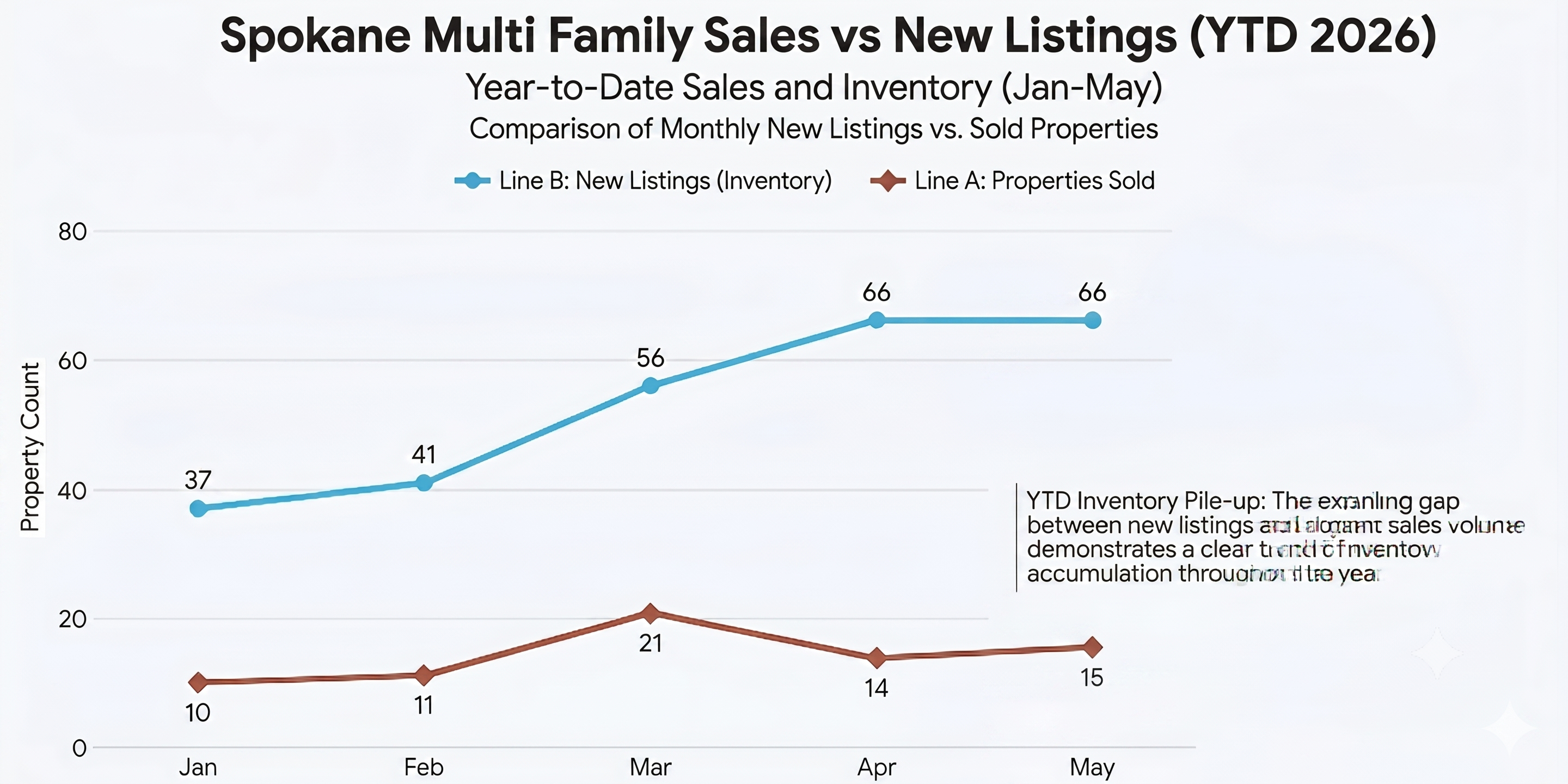

Spokane’s Systemic Supply Surge

The broader Spokane multi-family sector mirrors this trend, suggesting a regional economic hesitation rather than a niche property issue. Total new inventory in Spokane surged from 37 listings in January to a sustained plateau of 66 units in both April and May, a 78% increase in available stock.

In contrast, closed transactions remained largely flat. Aside from a brief uptick in March, monthly sales hovered between 10 and 15 units. This means that while the selection available to buyers nearly doubled over five months, the actual transaction volume barely moved. This suggests a systemic "wait-and-see" approach from institutional and private investors alike, likely driven by sensitivity to interest rates or a significant gap between asking prices and current appraisal values.

What I'm Seeing for Remaining 2026

As the increase in inventory is outpacing the sales, we are also seeing investor sentiment cool for those interested in Spokane area rental properties. As I'm talking with clientele, the legislative changes that have taken place over the last 24 months in favor of tenant protections at the cost of the investor, investors are waiting on the sidelines or finding other areas of the country to spend their investment dollars.

What the data doesn't show is the amount of shadow inventory available as many investors are seeking to liquidate their Spokane portfolios. They are waiting for increased demand as current prices aren't appealing to owners. Interest rates in the 7's for investment properties are affecting affordability for potential buyers and limiting the benefits of the DSCR loan. The DSCR loan is fast becoming the most attractive loan for Spokane investors as qualifications are based on the income of the property, rather than the borrower's financial abililty.

If sales volume does not begin to clear the backlog by July, the market may see the first significant wave of price corrections as sellers are forced to bridge the gap to meet buyer expectations. We are currently seeing properties sell at a CAP rate between 6-9%. I would expect the properties to be selling at a higher CAP as we get further into the year.